Résumé

Le Minage est le processus permettant aux transactions Bitcoin d'être vérifiées et ajoutées à la blockchain. L'objectif des mineurs est de trouver une solution à un problème mathématique complexe. Les mineurs qui parviennent à trouver la solution gagnent les nouveaux bitcoins et les frais de transaction.

À la création du Bitcoin, il suffisait d'un simple ordinateur portable pour miner du BTC. Aujourd'hui, ce processus nécessite du matériel bien spécifique. Le minage en solo étant difficile, de nombreux mineurs rejoignent des pools pour augmenter leur chances d'obtenir un bloc de récompense et divisent ensuite celui-ci.

Introduction

Le minage de bitcoins garantit le maintien de la légitimité des transactions survenant sur la blockchain. Il s'agissait, à l'époque, d'une solution unique pour créer la confiance dans un environnement sans confiance. En ce sens, le minage figure au cœur du modèle de sécurité du Bitcoin.

L'idée de miner et de recevoir des BTC en retour est une idée séduisante. S'il n'est plus possible de miner du BTC avec des processeurs, il n'est pas toujours nécessaire de posséder une machine pour miner des cryptos. Avant que vous ne décidiez si le minage est fait pour vous, précisons brièvement comment celui-ci fonctionne.

Qu'est-ce que le minage de bitcoins ?

Lorsqu'un utilisateur crée une nouvelle transaction sur la blockchain du bitcoin, il doit attendre que les autres utilisateurs du réseau (les nœuds) vérifient celle-ci. Les mineurs sont chargés de collecter les nouvelles transactions en attente et de les regrouper dans un bloc candidat (un nouveau bloc qui doit encore être validé).

L'objectif d'un mineur est de trouver le bon hash pour son bloc candidat. Le hash d'un bloc est une chaîne de chiffres et de lettres qui fonctionne comme un identifiant unique pour chaque bloc. Voici un exemple de hash :

0000000000000000000b39e10cb246407aa676b43bdc6229a1536bd1d1643679

Afin de créer un hash, le mineur doit rassembler le hash du bloc précédent, les données de son bloc candidat (un nonce), puis le soumettre via une fonction de hachage.

Néanmoins, le mineur doit trouver un nonce qui, une fois associé à toutes les données, générera un hash commençant par une certaine quantité de zéros. Le nombre de zéros dépend de la difficulté de minage. Le hash d'un bloc valide prouve que le mineur a bien effectué le travail nécessaire pour valider son bloc candidat (il s'agit de la Preuve de travail).

Après avoir collecté les transactions en attente et créé leur bloc candidat, le nonce est la seule chose qu'un mineur peut changer, c'est ce à quoi servent les rigs deminage. Dans le cadre d'un processus intensif d'essai et d'erreur, les rigs continuent de modifier le nonce et le hachage des données jusqu'à ce qu'elles trouvent une solution à ce bloc (c'est-à-dire un hash qui commence par une certaine quantité de zéros).

Dès qu'un mineur trouve un hash valide, il peut valider son bloc candidat et percevoir les bitcoins. C'est également à ce moment que les transactions de la blockchain incluses dans ce bloc sont confirmées.

Combien gagne un mineur de bitcoins ?

Chaque nouveau bloc offre au mineur une récompense de bloc, qui se compose de bitcoins (souscription de bloc) nouvellement générés, plus les frais de transaction. Vu que la récompense de bloc est presque entièrement constituée de la subvention de bloc, la plupart des gens la désignent comme la récompense de bloc (sans tenir compte des frais).

En ce qui concerne le Bitcoin, la subvention du bloc a commencé à 50 BTC en 2009 et est réduite de moitié tous les 210 000 blocs (environ quatre ans). Ces « halvings » ont entraîné une diminution de la récompense de validation de bloc à 25 BTC en 2012, puis à 12,5 BTC en 2016, et enfin à 6,25 BTC en 2020. Le prochain halving aura lieu en 2024. En mai 2021, la récompense par bloc donne aux mineurs environ 300 000 dollars par bloc.

Toutefois, il existe de nombreux facteurs à prendre en compte lors du calcul de la rentabilité. La vitesse à laquelle un rig peut produire des nonces aléatoires et les tester est une mesure importante à vérifier. Ce chiffre est connu sous le nom de taux de hachage, il est essentiel au succès d'un mineur de bitcoins. Plus le taux de hachage est élevé, plus vous serez en mesure de tester rapidement ces entrées aléatoires.

Une autre mesure importante est la consommation énergétique du rig. Si vous dépensez plus d'argent pour l'électricité que la valeur gagnée par le mining, la rentabilité est nulle.

Comment miner du Bitcoin

Étant donné que le Bitcoin est décentralisé et est open-source, tout le monde peut se joindre à la course au minage. Dans le passé, vous pouviez utiliser votre ordinateur personnel pour extraire de nouveaux blocs. Mais du fait de l'augmentation de la difficulté de minage, vous avez désormais besoin de machines plus puissantes (plus d'informations à ce sujet ci-dessous).

D'un point de vue théorique, vous pouvez toujours essayer de miner des bitcoins avec votre ordinateur personnel, mais les chances de trouver un hash valide sont quasiment nulles. Le calcul de la fonction de hachage est relativement rapide, mais le calcul de la quantité massive d'entrées aléatoires prend beaucoup plus de temps. C'est pourquoi vous avez maintenant besoin de matériel spécialisé avant même d'essayer de devenir un mineur rentable.

Quel équipement de minage dois-je utiliser ?

En général, vous pouvez essayer de miner des cryptomonnaies à l'aide d'un processeur, d'un GPU, d'un FPGA ou d'une machine ASIC (nous allons les aborder). Certains altcoins peuvent encore être minés avec des GPU. Les machines FPGA peuvent également être une option en fonction de l'algorithme de minage, de la difficulté et des coûts d'électricité. Néanmoins, quand il s'agit de Bitcoin, l'usage d'ASIC est fortement conseillé.

Processeur (unité centrale de traitement)

Les processeurs fonctionnent comme une puce permettant de distribuer des instructions sur différentes parties d'un ordinateur. Les processeurs ne sont aujourd'hui plus assez efficaces pour miner des cryptomonnaies.

GPU (unité de traitement graphique)

Les GPU peuvent servir à différentes fins, mais ils sont essentiellement utilisés pour traiter les données graphiques et les transmettre à l'écran. Ils peuvent diviser les tâches complexes en plusieurs tâches plus petites afin d'améliorer les performances. Certains altcoins peuvent être minés avec des GPU, mais l'efficacité dépend de l'algorithme de minage et de la difficulté.

FPGA (matrice de portes programmables in situ)

Les FPGA peuvent être programmés et reprogrammés pour servir différentes fonctions et applications. Ils sont personnalisables et plus abordables que les ASIC mais sont moins efficaces pour le minage de bitcoins.

ASIC (circuit intégré spécifique à une application)

ASIC signifie circuits intégrés spécifiques à une application, ce qui signifie que ces ordinateurs sont conçus pour un seul objectif. Les ASIC sont entièrement dédiées aux minage d'une cryptomonnaie. Les ASIC sont moins personnalisables et plus chers que les FPGA, mais leurs taux de hachage et leurs niveaux de consommation d'énergie en font l'option la plus efficace pour miner du bitcoin.

Pools de minage

Les chances de miner un bloc en étant seul sont extrêmement faibles. En rejoignant plutôt un pool de mining de cryptomonnaies, vous pouvez combiner votre puissance de calcul avec d'autres miners. Lorsque le pool réussit à extraire un bloc, chaque mineur reçoit une part des bitcoins minés. Les récompenses de la pool sont proportionnelles à la puissance de minage que vous offrez.

Comment rejoindre un pool de minage ?

Si vous rejoignez un pool en utilisant votre matériel localement, vous devrez configurer votre logiciel pour vous associer à d'autres mineurs. Le processus implique généralement la création d'un compte et la connexion au serveur du pool.

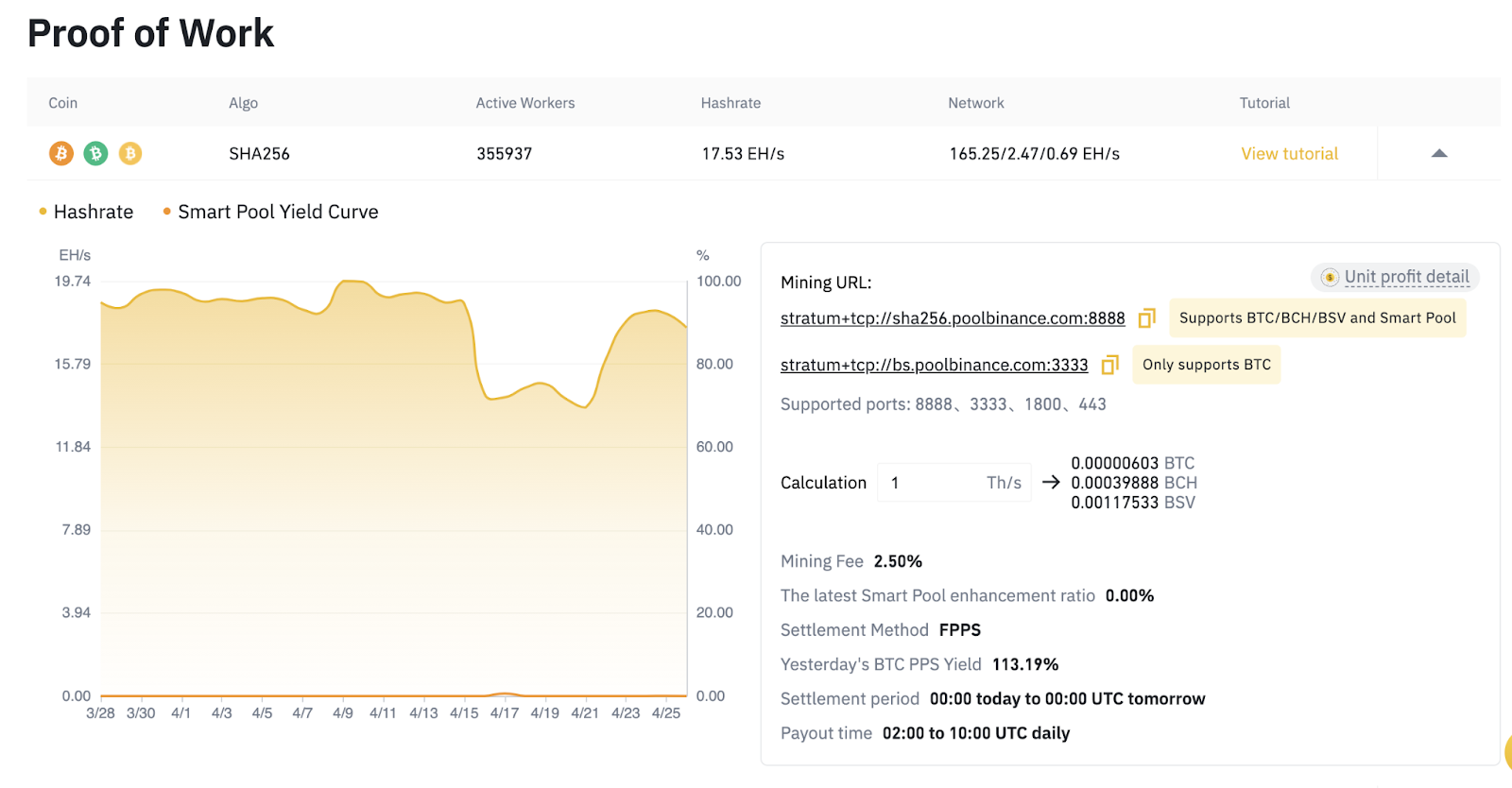

Si vous disposez d'un appareil de minage, la Binance Pool est un bon endroit pour commencer à miner des BTC et d'autres coins basées sur l'algorithme SHA-256. Votre ring passera automatiquement de BTC à BCH et BSV pour maximiser vos retours, qui sont payés en BTC.

Vous pouvez avoir une idée du bénéfice que vous pourriez obtenir en vous rendant sur la page Binance Pool. Les gains BTC sont versés quotidiennement dans votre portefeuille Bitcoin.

Minage sur le cloud (Cloud Mining)

Si vous souhaitez éviter les aspect les plus techniques, vous pouvez également rejoindre un pool de cloud mining, en laissant la gestion du matériel et des logiciels aux propriétaires de la ferme. D'une manière générale, le cloud mining consiste à payer quelqu'un pour qu'il mine en votre nom. Le propriétaire de la ferme devra alors partager les gains avec vous. Cependant, cette option est très risquée, car il n'y a aucune garantie que vous obtiendrez un retour sur investissement. De nombreux services de cloud mining s'avèrent être des escroqueries, alors soyez prudent.

Pour conclure

Disposer d'une compréhension de base du fonctionnement du minage de bitcoins vous pemettra de ne pas commettre d'erreurs. Avec la bonne combinaison de matériel et de logiciels, tout le monde peut commencer à miner et à contribuer à la sécurité du réseau Bitcoin. Même si vous réalisez que le minage n'est pas fait pour vous, vous pouvez toujours contribuer au réseau en exécutant un nœud Bitcoin.

L'investissement initial pour être rentable en minage est très élevé et de nombreux risques sont impliqués. Vos rendements dépendront également des conditions du marché et de facteurs externes tels que les prix de l'énergie et les améliorations matérielles. Assurez-vous de faire vos recherches avant de dépenser de l'argent pour vos appareils.